One of the biggest topics of conversation at Broker Fair last week was a company called Capital One Equities. According to many attendees and discussions on DailyFunder, merchants were being contacted and offered large lines of credit, often in the $625,000 range. The catch was that the merchant was required to make a deposit or complete another funding transaction before the line of credit would become available.

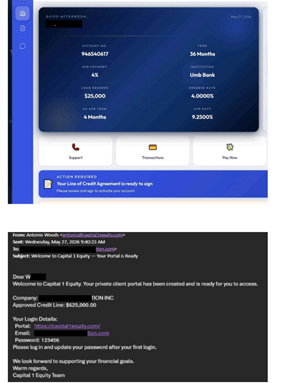

What raised even greater concern was that the company reportedly created an online portal where merchants could log in, create an account, deposit funds, and view what appeared to be an approved line of credit waiting for them.

The portal displayed an approved credit line of $625,000, creating the appearance that the funds were already available and simply awaiting activation. To many merchants, a portal like this can create a false sense of security and legitimacy.

Unfortunately, many industry veterans believe these lines of credit were never going to materialize.

This is not an isolated issue.

We recently discussed Blue Rock, which has been accused of using a similar approach. Merchants are promised a large line of credit after successfully completing a high-cost MCA. In many cases, the merchant accepts funding they cannot realistically afford because they are focused on the promise of a future $625,000 credit facility. Once the MCA is repaid, the promised line of credit never arrives.

This type of bait-and-switch continues to damage the reputation of the MCA industry and, more importantly, harms the very merchants we are supposed to be helping.

Educate Your Merchant

When a merchant tells you that they have been approved for a $625,000 line of credit, ask a few simple questions:

• Did the lender request two years of business tax returns?

• Did the lender request financial statements?

• Was collateral discussed?

• Was there any discussion about home equity or other assets?

• Based on the merchant’s credit profile and financial situation, does this approval realistically make sense?

Many merchants do not understand the underwriting process behind traditional bank lines of credit. If a business owner with challenged credit is suddenly being offered a large unsecured credit facility with little or no documentation, that should immediately raise concerns.

A legitimate lender extending a $625,000 credit facility is typically going to perform substantial due diligence. Financial statements, tax returns, bank statements, collateral reviews, and a detailed underwriting process are standard requirements. When those requirements are absent, merchants should proceed with extreme caution.

Education is the key.

As brokers, we have a responsibility to explain how legitimate lending works and to help merchants recognize offers that sound too good to be true. Unfortunately, no matter how many investigations, lawsuits, criminal cases, or prison sentences occur, there will always be individuals who are unwilling to learn how to sell properly and who instead rely on deceptive tactics.

The solution is not another regulation.

The solution is not another arrest.

The solution is education.

If you take the time to properly educate your merchants, you can help them avoid costly mistakes, save money, build trust, and remain long-term clients.

In an industry where relationships matter, educating your customers may be the most valuable service you can provide.